The United States (US) Bureau of Economic Analysis (BEA) will publish the first preliminary estimate of the fourth-quarter Gross Domestic Product (GDP) at 13:30 GMT.

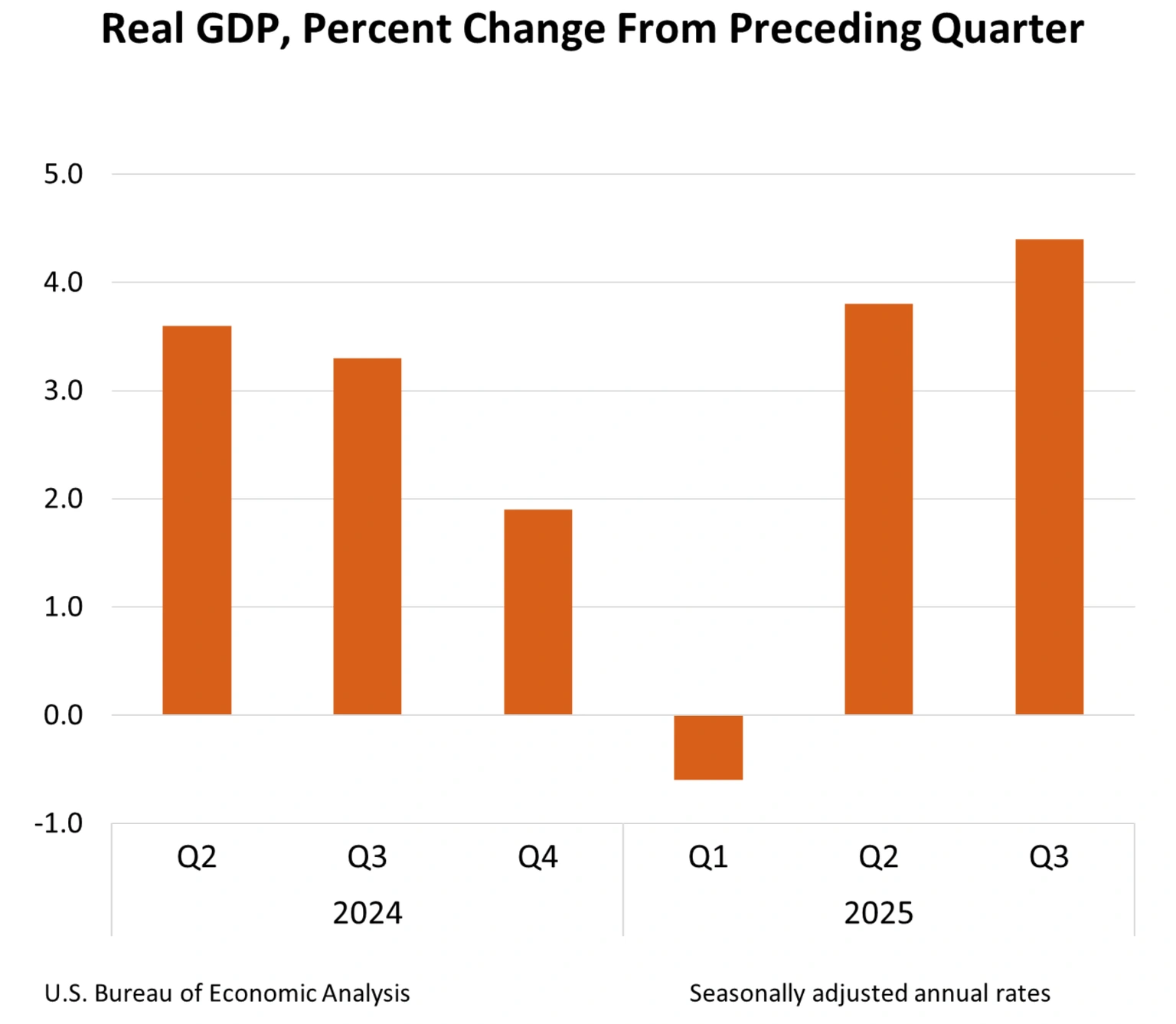

Analysts forecast the US economy to have expanded at a 3% annualized rate, slowing down from the 4.4% growth posted in the previous quarter, as the extended US government shutdown, extending from October to mid-November, hit economic growth.

Investors see US economic strength faltering in Q4

The US economy is expected to have switched a gear down in the last three months of 2025, following a surprising acceleration in the previous quarter. The 3% annualized GDP forecast is still revealing a healthy growth rate compared with other major economies, but it underscores some of the weaknesses seen in recent weeks and might dent the theory of US economic exceptionalism.

The US government shutdown is likely to have contributed to the economic slowdown. “We estimate real GDP grew at a 1.6% annualized pace in Q4, with most of the weakness attributable to the extended government shutdown from early October through mid‑November, which likely shaved roughly 1.2 percentage points from headline growth,” economists from Wells Fargo said in a research note. Stripping out the shutdown effects, the underlying fundamentals remain solid, they added.

Still, the labour market remains the main concern. January’s Nonfarm Payrolls revealed an unexpectedly strong increase in net jobs and a decline in unemployment, but nearly two-thirds of the new vacancies were concentrated in the health sector. Beyond that, employment data from 2025 was revised down to 181,000 from previous estimations of 584,000, far fewer than the 1.46 million jobs created in 2024.

Moreover, consumption, which accounts for nearly 70% of the GDP, is showing a worrying trend. Retail Sales stalled in December amid a decline in big-ticket sales, and data from October was downwardly revised. It seems that the uncertain employment expectations and a rising cost of living, due in part to trade tariffs, are starting to pinch on consumers’ sentiment, weighing on the economic growth.

Alongside the Q4 GDP, the US Bureau of Economic Analysis (BEA) will also release the preliminary US Personal Consumption Expenditures (PCE) Price Index data for December. The US Federal Reserve’s (Fed) preferred inflation gauge is expected to show that inflation remains sticky, closer to a 3% year-on-year growth than to the Fed’s 2% target rate. The risk is on a mix of low growth and hot inflation that would pose a headache for the Fed and might trigger wild US Dollar fluctuations.

When will the Gross Domestic Product print be released, and how can it affect the US Dollar Index?

The US GDP report is due at 13:30 GMT, alongside the US PCE Price Index report. Trading volumes have been subdued at the start of the week as investors await key economic releases at later dates. Bearing this in mind, it is likely that, if both readings point to the same monetary policy direction, they might have a significant impact on the US Dollar’s (USD) volatility.

Friday’s data is likely to be a test of the frail US Dollar recovery witnessed this week. The Euro (EUR) and the Japanese Yen (JPY) are losing momentum, and the Pound Sterling (GBP) struggles as soft UK economic growth and inflation figures have boosted hopes of BoE monetary easing in March. The Greenback, however, will need support from domestic data to confirm a trend shift.

Guillermo Alcalá, FX analyst at FXStreet.com, sees the higher low of the US Dollar Index (DXY) at the 96.50 area as a potential sign of bottoming, although bullish momentum remains tentative while below the 98.00 area: “Last week’s higher low at 96.50 is a good sign for the US Dollar, but bulls would need to break and hold above the 98.00 level to confirm a trend shift and set sail for the 98.85 area, where a descending trendline resistance meets the January 21 and 22 highs.”

“A combination of undershoot GDP growth and soft inflationary pressures, on the other hand, would prompt investors to ramp up bets of Fed rate cuts for 2026 and undermine speculative support for the US Dollar. “A reversal below 96.50 would put bears back in control, exposing the four-year low at 95.55 hit in January,” Alcalá adds.

US Dollar FAQs

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022.

Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates.

When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system.

It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

Economic Indicator

Gross Domestic Product Annualized

The real Gross Domestic Product (GDP) Annualized, released quarterly by the US Bureau of Economic Analysis, measures the value of the final goods and services produced in the United States in a given period of time. Changes in GDP are the most popular indicator of the nation’s overall economic health. The data is expressed at an annualized rate, which means that the rate has been adjusted to reflect the amount GDP would have changed over a year’s time, had it continued to grow at that specific rate. Generally speaking, a high reading is seen as bullish for the US Dollar (USD), while a low reading is seen as bearish.

Read more.

Read the full article here