Key takeaways

-

The EU’s new crypto tax rules do not introduce new taxes but expand tax transparency by ensuring that crypto transactions are reported and shared across member states.

-

Reporting obligations fall primarily on crypto-asset service providers, requiring them to collect user identity information, tax residency details and transaction data in a standardized format.

-

Information reported by platforms will be automatically exchanged among EU tax authorities, reducing cross-border reporting gaps for crypto users.

-

The framework aligns with the Organisation for Economic Co-operation and Development’s global crypto reporting standard, increasing compatibility with non-EU jurisdictions.

The European Union is set to significantly enhance its monitoring of cryptocurrency transactions for tax purposes. Starting Jan. 1, 2026, updated reporting obligations require crypto platforms operating in the EU or serving EU users to provide detailed information on users and their transactions to tax authorities. This change aligns digital assets more closely with the transparency requirements long established in conventional finance.

The key legislation driving this shift is Council Directive (EU) 2023/2226, commonly known as DAC8. It expands the EU’s existing framework for the automatic exchange of tax information to include crypto assets. Paired with the Markets in Crypto-Assets (MiCA) regulation, DAC8 represents a major step in regulating the crypto sector. It focuses specifically on taxation rather than solely on market conduct or licensing.

This article explains how the new EU crypto tax reporting system will work, outlines the obligations for platforms and examines the implications for individual users as the rules take effect.

Why DAC8 is being introduced: Closing the gap from banks to blockchains

For more than a decade, EU countries have used the Directive on Administrative Cooperation (DAC) to automatically share tax-related financial data across borders. Previous iterations covered bank accounts, investment income and certain digital platforms, but crypto transactions were largely exempt from routine reporting.

As cryptocurrency adoption grew in Europe, this exemption created clear loopholes for potential tax evasion. EU authorities viewed it as inconsistent to exempt crypto solely because of its technological basis.

DAC8 aims to close this gap by formally incorporating crypto assets into the tax transparency system, ensuring that transaction data is gathered, reported and exchanged in a manner similar to traditional financial information. The European Commission has emphasized that crypto deserves no special exemption from tax enforcement.

Alignment with the OECD’s Crypto-Asset Reporting Framework (CARF)

The EU built DAC8 around the CARF, which was launched in 2023. The CARF sets a global benchmark for crypto transaction reporting by specifying:

-

Which crypto assets qualify for reporting

-

Which entities must report

-

The specific user and transaction details required.

By adopting the CARF model, the EU promotes consistency with international standards, making it easier to share data with non-EU countries that implement similar rules.

Did you know? Before crypto-specific rules, several EU tax authorities relied on blockchain analytics firms instead of formal reporting to estimate crypto activity, often producing significantly different figures for the same market.

Scope of DAC8: Covered assets and platforms

The focus of DAC8 is on crypto-asset service providers (CASPs) operating in the EU. These include centralized exchanges, brokers, custodial wallets and similar intermediaries. The rules cover a broad range of assets, including most cryptocurrencies, stablecoins, tokenized assets and certain non-fungible tokens that function more like investment vehicles than pure collectibles. The emphasis is on transferability and investment use rather than on specific labels.

The obligations extend beyond EU-based platforms. Non-EU providers serving EU users may also need to comply, highlighting the directive’s extraterritorial impact.

Timeline and implementation of DAC8

Adopted in October 2023, DAC8 required transposition into national law by Dec. 31, 2025, with application starting on Jan. 1, 2026. As of early 2026, some member states have faced delays or infringement notices for incomplete transposition, though the EU expects full enforcement.

Key dates include:

-

Platforms began collecting relevant data on Jan. 1, 2026.

-

The first reports, covering 2026 activity, will be submitted to national tax authorities in 2027, typically within nine months of year-end.

-

Tax authorities then automatically exchange the data annually with other EU countries.

The commission has signaled that it expects timely and full implementation. Several countries have received formal notices for delays in transposing the rules, underlining that enforcement will not be optional.

Did you know? Early drafts of EU crypto tax proposals debated whether self-custody wallets could ever be subject to reporting, highlighting how difficult it is to regulate decentralized ownership.

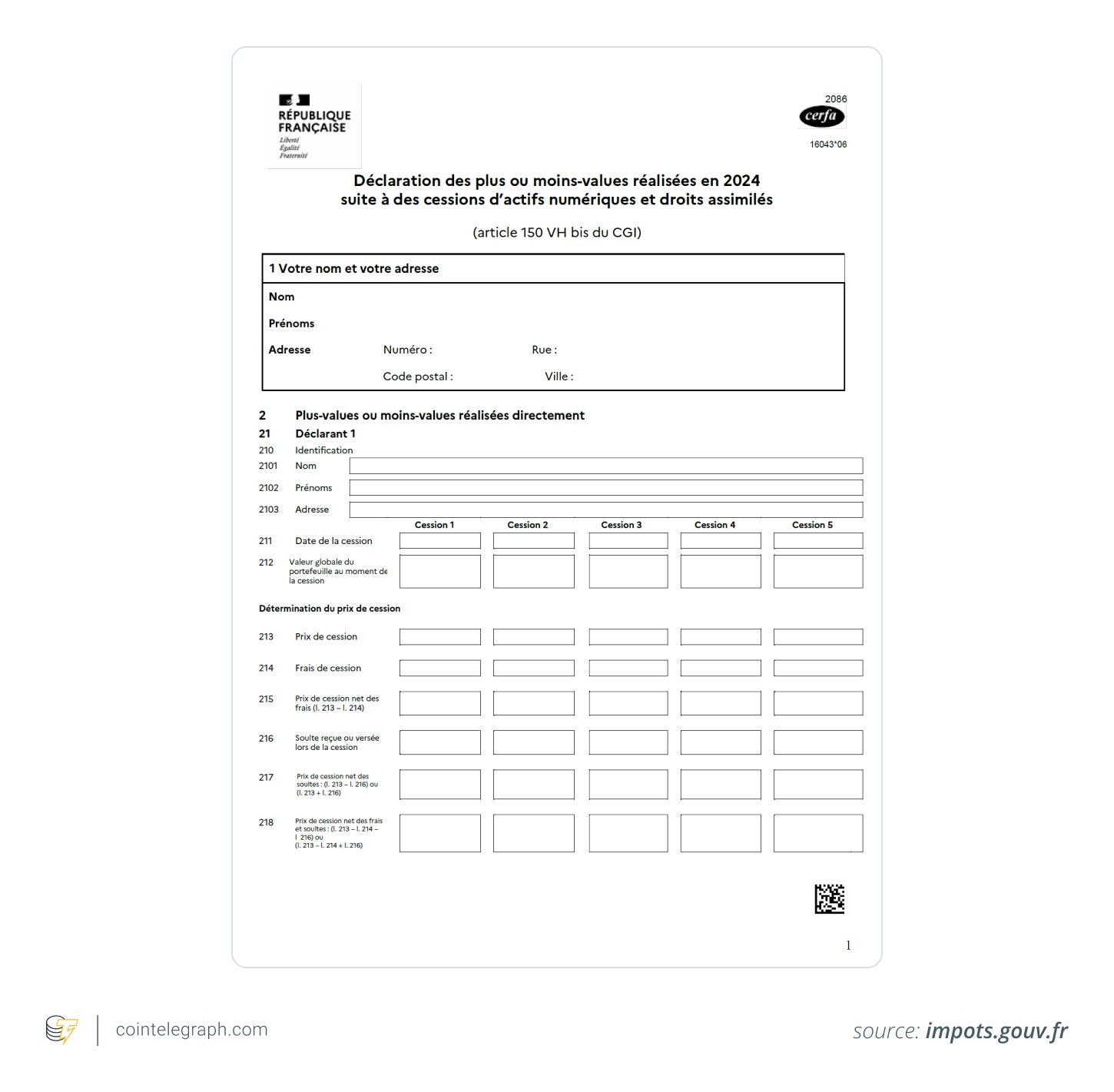

Reporting requirements for platforms in DAC8

Under DAC8, CASPs are required to perform enhanced due diligence and submit detailed information to their local tax authority. This includes user details such as full name, address, tax residency and tax identification number (TIN), if available.

Transaction data includes:

-

Types of crypto transactions, such as sales, exchanges and transfers

-

Gross proceeds from disposals

-

Dates and values of transactions.

After collection, this information is automatically shared among EU tax authorities. A user’s country of residence receives the relevant data even if the platform is located in a different country.

For platforms, DAC8 makes crypto tax reporting a structured, recurring compliance obligation. It more closely resembles financial reporting than ad hoc disclosures.

Impact of DAC8 on crypto users

One of the most significant changes for crypto users is increased tax reporting transparency under DAC8. National tax authorities can now view transactions conducted on reporting platforms.

This may result in:

-

Requests for more detailed tax residency or identification information during account setup or updates

-

Greater ability for authorities to match crypto activity against declared income on tax returns

-

Easier detection of inconsistencies between reported data and tax filings.

DAC8 does not introduce new taxes or standardize rates across the EU. Member states retain authority over crypto taxation policies, as the directive focuses solely on information exchange. While DAC8 automates data exchange between authorities, users are still required to report their crypto activity through their respective national tax returns.

Compliance challenges for platforms under DAC8

Implementing DAC8 requires significant upgrades, including accurate transaction tracking, tax residency verification and secure data storage. Smaller or less-resourced providers may struggle to meet these obligations alongside MiCA and Anti-Money Laundering requirements.

Non-compliance carries the risk of penalties, including fines for late, incomplete or missing reports. Some platforms have indicated that regulatory compliance costs may influence where they choose to operate.

Users may also face confusion in understanding DAC8 in the context of MiCA. DAC8 addresses tax transparency behind the scenes, while MiCA covers licensing, investor safeguards and market conduct.

The two are complementary: DAC8 ensures tax data flows once services are active, while MiCA defines permissible operations. Together, they create a comprehensive oversight framework for the crypto economy.

Certain aspects remain unclear under DAC8, such as how decentralized finance (DeFi) fits in when no central intermediary exists to report to. Privacy advocates have raised concerns about extensive data collection and sharing, though EU officials note that the General Data Protection Regulation (GDPR) and other data protection laws continue to apply. It remains to be seen how these safeguards will operate in practice.

Did you know? Similar crypto tax reporting models are being explored in Asia-Pacific and Latin America, suggesting that EU-style transparency could become a global norm rather than a regional exception.

DAC8 in the broader context

DAC8 forms part of a global trend as crypto integrates into mainstream finance. Governments worldwide are increasingly treating it as part of the mainstream financial system rather than as a parallel economy viewed with suspicion.

By adopting OECD-aligned standards and enabling cross-border exchanges, the EU underscores that crypto will face the same transparency demands as traditional assets. For users and platforms in Europe, the period of limited formal tax oversight is effectively ending.

Cointelegraph maintains full editorial independence. The selection, commissioning and publication of Features and Magazine content are not influenced by advertisers, partners or commercial relationships.

Read the full article here