After Friday’s revelation that it was the first consecutive monthly Friday 13th for 11 years, DB’s Jim Reid writes that today’s nearly-as-impressive revelation is that this week sees the Fed, ECB, BoJ and BoE all meet in a single calendar week for the first time since December 2021. So a “super week” for central banks. All of them will have a very complex backdrop to deal with, shaped by geopolitical risk, volatile energy prices, and unsettled inflation dynamics.

Clearly the Middle East is the center of attention for markets right now, with oil prices fluctuating rapidly depending on the mood of the moment, which in turn is set by rapid burst headlines which are stale by the time the next flashing red headline hits. And since every asset class now reacts to any up or down tick in oil, it leads to cross-asset chaos, to say the least. The bigger problem, of course, is that the longer the conflict lasts, and the higher oil prices rise, the more hawkish central banks will have to be no matter the AI-driven bloodbath in the labor market.

Indeed, while the Iran war is set to dominate the week ahead, we do still have those four big central bank meetings, where all eyes will be on their reaction functions to the war’s impact and the latest oil shock. Starting with the Fed, DB economists expect them to keep rates unchanged this week and think they’ll emphasize elevated geopolitical uncertainty. They only expect minor statement tweaks, including smoothed language on recent labor data (especially given January and February’s conflicting payrolls) and a nod to geopolitical risks, highlighting uncertainty and near-term upside pressure on inflation. Then at the press conference, they think Chair Powell is likely to stress that recent events mainly transmit through financial conditions—particularly oil prices. For now, however, economists think he’ll avoid signalling any meaningful shift in the near term policy outlook.

For the Fed, an important consequence of the conflict is that higher energy prices have begun to feed into inflation assumptions. So DB’s economists have nudged up their headline inflation estimates for this year, and they expect Fed officials to reflect a similar adjustment when they publish their updated Summary of Economic Projections. Indeed, core PCE inflation has registered back-to-back 0.4% monthly increases now, pushing the year-on-year rate to 3.1%, the highest since early 2024. For the dot plot, economists are still expecting it to signal one rate cut this year, although it wouldn’t take much to shift the median dot for 2026. Clearly though, the outlook is going to remain heavily dependent on the oil price. For example, our economists have found that a sustained oil price around $100/bbl would still see the projected tax benefits to consumers from the One Big Beautiful Bill Act outweigh the drag from higher effective energy costs. However, a move toward $150/bbl would pose a more material risk to consumer spending and the broader outlook.

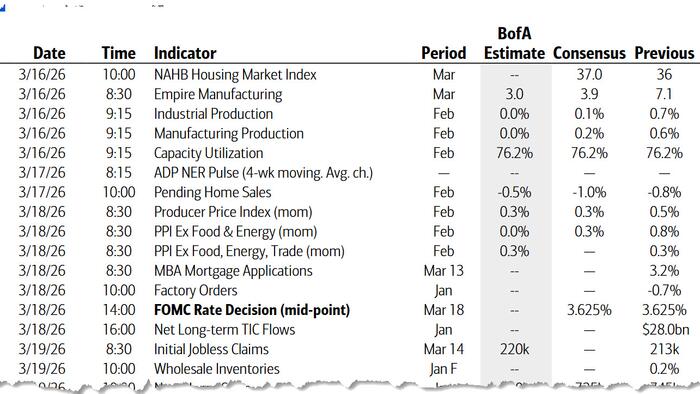

Beyond the Fed, this week’s incoming data is unlikely to materially alter the tone of the meeting. February’s industrial production today is expected to rise by 0.3%, slower than January’s 0.7%, largely due to softer utility output, though oil and gas extraction will be worth monitoring. Otherwise, the regional manufacturing surveys from New York and Philadelphia could reflect some drag from geopolitical uncertainty, with particular attention on capital spending components. And given the recent labor market volatility, Thursday’s initial jobless claims will take on added importance as they fall within the March employment survey window.

Away from the US, this Thursday will bring the ECB, BoE and BoJ meetings, with DB economists expecting all three to leave rates on hold, with the emphasis firmly on guidance rather than action. At the ECB, expect the Governing Council to acknowledge heightened uncertainty and near-term upside risks to inflation, while stopping short of explicitly flagging medium term risks. Also expect a strong reiteration of policy flexibility and a clear message underscoring the ECB’s unwavering commitment to price stability, with officials keen to signal that they stand ready to act to avoid a repeat of the 2022–23 inflation episode.

Then in the UK, DB thinks the MPC will lean into a dovish wait and see stance amid a more clouded outlook following the Iran related energy shock. Expect a less divided vote than in February, with the majority favoring an unchanged Bank Rate, while two members continue to favor a cut. Although DB economists still sees two rate cuts this year, recent developments have pushed back the expected timing.

Over in Japan, the BoJ is expected to maintain its current stance, with attention focused on Governor Ueda’s press conference. While underlying fundamentals could justify an early hike, elevated oil prices and growth risks are likely to temper near term action, and sustained crude prices above $100/bbl would reduce the likelihood of an April move. Meanwhile, other central banks making decisions this week include the RBA (Tuesday; expect a hike), the BoC (Wednesday), the SNB and the Riksbank (Thursday). The latter three are widely expected to see no change in rates.

Finally this week, notable data includes Germany’s Zew survey for March tomorrow and UK labor market data due Thursday. In the geopolitical sphere, President Trump and Japanese PM Takaichi are meeting in Washington, with defence cooperation expected to be the primary topic (see more in our Chief Japan economist’s week ahead here). In Europe, this week’s events include an EU leaders’ summit (Thursday to Friday). And on earnings, the lineup includes Micron, FedEx and Lululemon in the US as well as Tencent and Alibaba in China. See the day-by-day calendar of events at the end as usual for more.

Courtesy of DB, here is a day-by-day calendar of events

Monday March 16

- Data: US March Empire manufacturing index, NAHB housing market index, February industrial production, capacity utilisation, China February retail sales, industrial production, home prices, investment, Italy January general government debt, Canada February CPI, housing starts

- Earnings: Standard Life

- Other: EU foreign affairs council meeting

Tuesday March 17

- Data: US March New York Fed services business activity, February leading index, pending home sales, Germany March Zew survey, Eurozone March Zew survey, Canada February existing home sales

- Central banks: RBA decision

- Earnings: Lululemon, Oklo

- Auctions: US 20-yr Bond (reopening, $13bn)

Wednesday March 18

- Data: US February PPI, January factory orders, total net TIC flows, Japan January Tertiary industry index, February trade balance, Canada January international securities transactions

- Central banks: Fed decision, BoC decision

- Earnings: Tencent, Micron

Thursday March 19

- Data: US March Philadelphia Fed business outlook, January new home sales, wholesale trade sales, initial jobless claims, UK January average weekly earnings, unemployment rate, February jobless claims change, Japan January core machine orders, capacity utilisation, Eurozone January construction output, Q4 labour costs, Australia February labour force survey

- Central banks: rate decisions from the ECB, the BoJ, the BoE, the SNB and the Riksbank

- Earnings: Alibaba, Accenture, Enel, FedEx, Vonovia

- Auctions: US 10-yr TIPS (reopening, $19bn)

- Other: Leaders of US and Japan meet in Washington, European Council meeting (through Friday)

Friday March 20

- Data: UK February public finances, Germany February PPI, Italy January trade balance, current account balance, ECB January current account, Eurozone January trade balance, Canada January retail sales, February industrial product price index, raw materials price index

- Central banks: China 1-yr and 5-yr loan prime rates, ECB’s Nagel speaks

* * *

Finally, looking at just the US, the key economic data release this week is the PPI report on Wednesday. The March FOMC meeting is on Wednesday. The post-meeting statement will be released at 2:00 PM ET, followed by Chair Powell’s press conference at 2:30 PM.

Monday, March 16

- 08:30 AM Empire State manufacturing survey, March (consensus +3.9, last +7.1)

- 09:15 AM Industrial production, February (GS flat, consensus +0.1%, last +0.7%); Manufacturing production, February (GS +0.1%, consensus +0.1%, last +0.6%); Capacity utilization, February (GS 76.1%, consensus 76.2%, last 76.2%): We estimate industrial production was unchanged in February, reflecting strong auto production but weak electricity production. We estimate capacity utilization edged down to 76.1%.

- 10:00 AM NAHB housing market index, March (consensus 37, last 36)

Tuesday, March 17

- 10:00 AM Pending home sales, February (GS flat, consensus -0.7%, last -0.8%)

Wednesday, March 18

- 08:30 AM PPI final demand, February (GS +0.4%, consensus +0.3%, last +0.5%); PPI ex-food and energy, February (GS +0.3%, consensus +0.3%, last +0.8%); PPI ex-food, energy, and trade, February (GS +0.3%, consensus +0.3%, last +0.3%); 10:00 AM Factory orders, January (GS +0.1%, consensus +0.1%, last -0.7%) : We forecast that factory orders increased by 0.1% in January, driven by a rebound in commercial aircraft orders.

- 02:00 PM FOMC statement, March 17-18 meeting: As discussed in our FOMC preview, we expect the FOMC to leave the funds rate unchanged at 3.50–3.75%. We expect Governors Bowman, Miran and Waller to dissent in favor of a 25bp cut. The Committee is likely to note in its statement that the war in Iran has increased uncertainty about the outlook and will likely raise inflation and weigh on economic activity in the near term. The Summary of Economic Projections is likely to show changes to the 2026 forecasts in line with our own, including higher core (+0.2pp to 2.7% Q4/Q4) and headline (+0.6pp to 3.0%) inflation, lower GDP growth (-0.2pp to 2.1%), and a higher unemployment rate (+0.2pp to 4.6%). We expect little change in the dot plot, where the median is likely to continue to show one cut in each of 2026 and 2027. We recently pushed the two additional rate cuts in our forecast back to September and December.

Thursday, March 19

- 08:30 AM Initial jobless claims, week ended March 14 (GS 210k, consensus 215k, last 213k); Continuing jobless claims, week ended March 7 (consensus 1,850k, last 1,850k): We expect initial jobless claims to decline by 3k. Initial claims remain below their average level in 2025H2 and the layoff rate edged down in January, suggesting that nationwide layoffs remain low despite the increase in alternative layoff measures in Q4 of last year.

- 08:30 AM Philadelphia Fed manufacturing index, March (GS 7.0, consensus 10.0, last 16.3)

- 10:00 AM New home sales, January (GS -2.0%, consensus -2.7%, last -1.7%): We estimate that new home sales fell by 2.0% in January, reflecting a drag from winter storm Fern.

Friday, March 20

- There are no major data releases scheduled.

Source: DB, Goldman

Read the full article here