Key Events This Week: PPI, Iran Talks, Nvidia Earnings, Fed Speakers Galore And State Of The Union

While much digital ink has been spilled on the Supreme Court’s striking down of Trump’s IEEPA tariffs and the consequences of this decision (see “Full Analysis Of The Supreme Court IEEPA Decision: How It Impacts The Economy, Policy And Markets“), a lot more is on deck for this week when we will also have more geopolitical headlines to contend with, as the latest round of US-Iran talks is expected in Geneva on Thursday. The talks come amid a recent buildup of US forces in the region and yesterday the New York Times was the latest outlet to report that Trump is considering an initial targeted strike against Iran in the coming days, which could be followed by a larger attack if Iran does not give in to US nuclear demands. Other highlights for the week ahead include the State of the Union address in the US (late tomorrow), US PPI and preliminary CPIs in Europe (both Friday). In earnings, the focus will be on Nvidia, Salesforce (both Wednesday) and Home Depot (tomorrow). Nvidia’s earnings could be the most important of these but expect lots of headlines from the State of the Union speech.

Friday’s US PPI release – where headline and core inflation are both forecast at 0.3% – will matter less in isolation than for its implications for the core PCE deflator. While January CPI surprised to the downside, the implications for core PCE continue to appear less favorable, with DB economists currently looking for a 0.4% monthly increase. Depending on the strength of key PPI components such as medical services, airfares, and portfolio management fees, a 0.5% increase in January core PCE cannot be ruled out, which would lift the year-over-year rate to around 3.1%. So an important release, especially in the sub-components.

There is a fair degree of Fed speak this week, with Waller (today and tomorrow) a highlight given he dissented in favor of a 25bps cut in January due to concerns over the labor market. However, we’ve subsequently seen a firm January jobs report and a firm December core PCE print, so will he shift his stance a bit? See the day-by-day week ahead at the end as usual for the rest of the Fed speakers and the key global data.

Elsewhere in the world, we have the German Ifo today and the preliminary European February CPI prints including for countries such as Germany, France and Spain, among others, on Friday. There will also be economic sentiment measures for key economies including consumer confidence in the UK, Germany and France, as well as the ECB’s consumer expectations survey due Friday.

Over in Asia, it’s a busy week ahead for Japan with key releases including the Tokyo CPI for February and the January industrial production both due on Friday. Our Chief Japan Economist expects core CPI inflation (ex. fresh food) of 1.7% YoY (2.0% in January) and core-core CPI inflation (ex. fresh food and energy) of 2.4% (2.4% in January). For industrial production, he sees a robust 4.5% MoM gain. See more in his full week-ahead here. Elsewhere, inflation will also be in focus in Australia and our economists expect a -0.2% MoM headline print and a 0.24% MoM trimmed mean print.

Other than Nvidia on Wednesday, other tech firms reporting include Salesforce, Intuit, Snowflake and CoreWeave. Amongst US consumer firms, the focus will be on Home Depot, TJX and Lowe’s. Over in Europe, there will be results from HSBC and Allianz in financials as well as other large firms such as Deutsche Telekom, Schneider Electric, Iberdrola and Rolls-Royce.

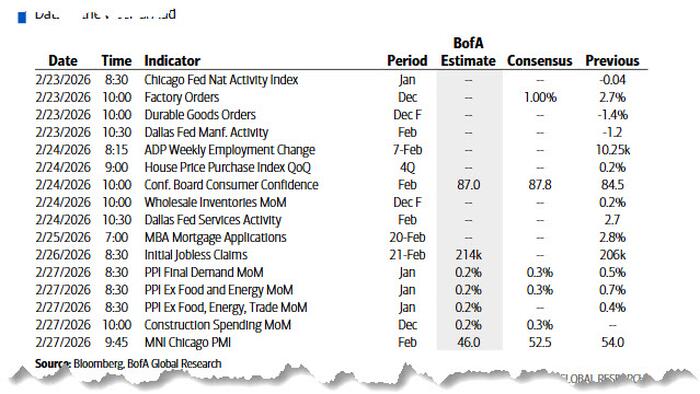

Courtesy of DB, here is a day-by-day calendar of events

Monday February 23

- Data: US January Chicago Fed national activity index, December factory orders, February Dallas Fed manufacturing activity, Germany February Ifo survey

- Central banks: Fed’s Waller speaks, ECB’s Lagarde speaks, BoE’s Taylor speaks

- Earnings: Dominion Energy, Domino’s Pizza

Tuesday February 24

- Data: US February Conference Board consumer confidence index, Dallas Fed services activity, Richmond Fed manufacturing index, business conditions, Philadelphia Fed non-manufacturing activity, December FHFA house price index, wholesale trade sales, Q4 house price purchase index, China January 1-yr and 5-yr loan prime rates, France February business confidence, EU27 January new car registrations

- Central banks: Fed’s Goolsbee, Collins, Bostic, Waller, Cook and Barkin speak, ECB’s Kocher speaks

- Earnings: Home Depot, Constellation Energy, MercadoLibre, American Tower, Standard Chartered, NRG Energy, Workday, Axon Enterprise, Fidelity National Information, MTU Aero Engines, First Solar, Telefonica, Amer Sports, CoStar, HP

- Auctions: US 2-yr Notes ($69bn)

- Other: US President Trump’s State of the Union address

Wednesday February 25

- Data: Japan January PPI services, Germany March GfK consumer confidence, France February consumer confidence, January retail sales, Australia January CPI

- Central banks: Fed’s Barkin and Musalem speak, ECB’s Vujcic speaks

- Earnings: NVIDIA, HSBC, TJX, Salesforce, Lowe’s, Iberdrola, Synopsys, Medline, Snowflake, E.ON, Diageo, Ferrovial, Haleon, Heidelberg Materials, Alcon, Leonardo, Trip.com, Sandoz, Wolters Kluwer, Paramount Skydance

- Auctions: US 2-yr FRN (reopening, $28bn), 5-yr Notes ($70bn)

Thursday February 26

- Data: US February Kansas City Fed manufacturing activity, initial jobless claims, Italy February consumer confidence index, economic sentiment, manufacturing confidence, Eurozone January M3, February economic confidence, Canada Q4 current account balance

- Central banks: ECB’s Lagarde and Dolenc speak, BoJ’s Takata speaks, BoE’s Lombardelli speaks

- Earnings: Deutsche Telekom, Schneider Electric, Allianz, Rolls-Royce, Intuit, AXA, Munich Re, Dell, Engie, Warner Bros Discovery, Eni, London Stock Exchange Group, Rocket, Erste, Cie de Saint-Gobain, CoreWeave, Autodesk, Baidu, Rocket Lab, Block, Zscaler, Stellantis, Flutter Entertainment

- Auctions: US 7-yr Notes ($44bn)

Friday February 27

- Data: US January PPI, February MNI Chicago PMI, Kansas City Fed services activity, December and November construction spending, UK February GfK consumer confidence, Lloyds Business Barometer, Japan February Tokyo CPI, January retail sales, industrial production, housing starts, Germany February CPI, unemployment claims rate, January import price index, France February CPI, January consumer spending, PPI, Q4 total payrolls, Italy December industrial sales, Canada Q4 GDP, Sweden Q4 GDP, Switzerland Q4 GDP

- Central banks: ECB January consumer expectations survey, BoE’s Pill speaks

- Earnings: Holcim, BASF, Swiss Re, Amadeus IT

Finally, looking at just the US, Goldman writes that the key economic data release this week is the PPI report on Friday. There are several speaking engagements with Fed officials this week, including events with Governors Waller, Cook, and Bowman.

Monday, February 23

- 08:00 AM Fed Governor Waller speaks: Fed Governor Christopher Waller will give a keynote address at the annual NABE economic policy conference. Speech text and Q&A are expected. On January 30, Waller said, “With total inflation excluding tariff effects close to our target at just slightly above 2 percent and a weak labor market, the policy rate should be closer to neutral, which the median FOMC participant estimates is 3 percent, and not where we are—50 to 75 basis points above 3 percent.”

- 10:00 AM Factory orders, December (GS -0.5%, consensus -0.7%, last +2.7%)

Tuesday, February 24

- 08:00 AM Chicago Fed President Goolsbee (FOMC non-voter) speaks; Chicago Fed President Austan Goolsbee will speak at the annual NABE economic policy conference. Q&A is expected. On February 17, Goolsbee said, “If…we can show that we’re on path to 2% inflation, I still think there’s several more rate cuts that can happen in 2026. But we’ve got to see it in coming data.”

- 09:00 AM Boston Fed President Collins (FOMC non-voter) speaks; Boston Fed President Susan Collins will give opening remarks at a Boston Fed conference on finance and payments.

- 09:00 AM Atlanta Fed President Bostic (FOMC non-voter) speaks; Atlanta Fed President Raphael Bostic will participate in a moderated discussion on monetary policy and the economic outlook. On February 20, Bostic said, “Our economy has remained remarkably resilient… [which] means that we have to worry about the implications for prices on a strong economy given inflation at around 3% is a long way from the 2% target.”

- 09:00 AM S&P Case-Shiller home price index, December (GS +0.3%, consensus +0.4%, last +0.5%)

- 09:00 AM FHFA house price index, December (consensus +0.3%, last +0.6%)

- 09:15 AM Fed Governor Waller speaks: Fed Governor Christopher Waller will give a keynote address at a Boston Fed conference on finance and payments. Speech text and Q&A are expected.

- 09:30 AM Fed Governor Cook speaks: Fed Governor Lisa Cook will participate in panel discussion on AI at the annual NABE economic policy conference. Speech text and Q&A are expected. On February 4, Cook said, “There is an argument for being optimistic about the path of inflation, but, until I see stronger evidence that inflation is moving sustainably back down to target, that is where my focus will be, in the absence of unexpected changes in the labor market.”

- 10:00 AM Conference Board consumer confidence, February (GS 87.0, consensus 87.0, last 84.5)

- 10:00 AM Wholesale inventories, December final (consensus +0.2%, last +0.2%)

- 03:15 PM Boston Fed President Collins (FOMC non-voter) and Richmond Fed President Barkin (FOMC non-voter) speak: Boston Fed President Susan Collins and Richmond Fed President Tom Barkin will participate in a panel discussion at a Boston Fed conference on finance and payments.

Wednesday, February 25

- There are no major economic data releases scheduled.

- 10:40 AM Richmond Fed President Barkin (FOMC non-voter) speaks: Richmond Fed President Tom Barkin will participate in a moderated Q&A panel at the Northern Virginia Chamber of Commerce. On February 4, Barkin said, “I think of the three cuts as having taken out some insurance to support the labor market as we work to complete the last mile to bring inflation back to target.”

- 11:00 AM Kansas City Fed President Schmid (FOMC non-voter) speaks: Kansas City Fed President Jeff Schmid will participate in a fireside chat about monetary policy and the economic outlook. On February 11, Schmid said, “Further rate cuts [would] risk allowing high inflation to persist even longer.”

- 01:20 PM St. Louis Fed President Musalem (FOMC non-voter) speaks: St. Louis Fed President Alberto Musalem will speak on the role of the Fed in the St. Louis region at the Missouri Athletic Club. Q&A is expected. On February 20, Musalem said, “A neutral real rate [right now] is appropriate, in my opinion, given my outlook for the economy… Policy is in a good place currently.”

Thursday, February 26

- 08:30 AM Initial jobless claims, week ended February 21 (GS 220k, consensus 215k, last 206k); Continuing jobless claims, week ended February 14 (consensus 1,863k, last 1,869k)

- 10:00 AM Fed Vice Chair for Supervision Bowman speaks: Fed Vice Chair for Supervision Michelle Bowman will testify before the Senate Banking Committee on bank supervision. Speech text and Q&A are expected. On January 30, Bowman said, “My view is that we should continue to focus on downside risks to our employment mandate. History tells us that the labor market can appear to be stable right up until it isn’t.” She also said, “I continue to see policy as moderately restrictive, and, looking ahead to 2026, my Summary of Economic Projections includes three cuts for this year.”

Friday, February 27

- 08:30 AM PPI final demand, January (GS +0.3%, consensus +0.3%, last +0.5%); PPI ex-food and energy, January (GS +0.4%, consensus +0.3%, last +0.7%); PPI ex-food, energy, and trade, January (GS +0.3%, last +0.4%)

- 10:00 AM Construction spending, December (GS +0.5%, consensus +0.2%, last +0.5% [October]); Construction spending, November (GS +0.4%)

Source: DB, Goldman

Loading recommendations…

Read the full article here