Submitted by Peter Tchir of Academy Securities

ProSec 2026

We will do a “traditional” outlook for 2026, covering all major markets, but we really wanted to highlight ProSec and define more carefully what we think it means for you as corporations, policy makers, and asset managers.

Production for Security:

-

RESILIENCY. We haven’t used the word “resiliency” as much as we could have and will use it more going forward. Being resilient, whether at the nation, state, or corporate level, will become a fixture in decision making.

-

ProSec is already in the process of supplanting “traditional” ESG as an overarching theme in decision-making and planning.

-

As much as we’ve tried to instill our view on how big, broad, and important the scope of ProSec is, we have failed to do that – so far.

-

While not critical to ProSec we do believe that as the world adopts a “Pre-War” mentality, it helps accelerate ProSec as it imbues a degree of “sacrifice for the greater good” while also imparting a sense of “urgency.”

-

ProSec is already going global and getting left behind on this initiative will be problematic for countries, companies, and investors.

Resiliency as a Driving Force Behind ProSec

To some degree we can describe ProSec as being the answer to “What If?”

-

What if global shipping is disrupted?

-

It has happened for reasons “out of our control.” COVID was not on anyone’s radar screen. Even the Evergreen blocking the Suez Canal was an “unforeseen” accident. Will markets react the same the next time around to companies exposed to that risk? What if some companies have “planned” for this and have more robust supply chains – less use of shipping, using a variety of shipping lanes, only shipping with countries they are very close to – physically or politically? If a “competitor” has prepared and you haven’t, and it occurs again, it is difficult to see markets being as “understanding” as they were when it was deemed farfetched.

-

Legend has it that the disaster recovery plan for one incredibly large hedge fund was to use other offices as disaster recovery sites. It had the advantage of being global, so if something happened in a region that took out the main office, and the disaster recovery site, it would still be covered. It had the advantage of all sites being up to date. Nothing worse than getting to the disaster recovery site and realizing that the internet is too slow and you were running obsolete versions of software. The plan made a lot of sense. It did not cover the contingency of grounding all U.S. flights for days. To the extent the story is true (and I have no reason to doubt it), I can assure you that this fund revamped their plans to cover even more contingencies as well as other highly unlikely, but still possible scenarios. They increased their RESILIENCY as they absorbed new information.

-

-

-

It happened because a “bad actor” behaved badly. Prior to the invasion of Ukraine by Russia, we could explain being “asleep at the switch” in terms of this type of risk. Iran and its proxies attacking more aggressively in the Middle East has not caused major disruptions, but it has caused some level of disruption, and seemed like a more foreseeable event than Russia’s invasion. The U.S. has just “blockaded” Venezuela. Actually, we did not “blockade” Venezuela as that is an act of war according to international law, but we have changed the nature of doing business with Venezuela.

-

The People’s Armed Forces Maritime Militia (PAFMM). We used GROK for some of this information, but it is all very consistent with topics we’ve discussed in the past. Let’s start with this map from GROK attributed to npr.org to explain some potential risks.

It (PAFMM) often operates in coordination with the PLA Navy (PLAN) and China’s Coast Guard (CCG) as part of a “joint defense” approach involving military, law enforcement, and civilian elements. In peacetime, it contributes to gray-zone tactics—coercive actions short of open warfare—such as swarming disputed features, harassing foreign vessels, or establishing a de facto presence to bolster territorial claims in the South China Sea and East China Sea. Western analyses describe it as enabling China to advance its interests while maintaining plausible deniability, as vessels appear to be civilian. Chinese sources emphasize its role in leading fishing activities, collecting oceanic information, supporting island/reef construction, and participating in drills for national defense and disaster relief. They have had as many as 400 ships active at any one time. According to GROK the “professional” component consists of 100-200 purpose-built boats (presumably larger and more sophisticated ones). There have been estimates that the total number of ships available is in the thousands. While not set up to attack, in the traditional sense, they can make sea travel perilous, not only by getting in the way, but also by dumping things like nets and logs overboard to foul propellors, etc.

The main focus today is Taiwan, because of our dependance on Taiwan for chips (a recurring theme of our 2026 Outlook), but it seems almost naïve to believe that there isn’t a bigger risk to shipping than just the concern around Taiwan’s chips (which in and of itself is a risk unless we become more “resilient” or diverse in our chip businesses).

We didn’t even touch on China’s control, ownership, and equipment in many ports across the globe as a potential future risk, but it certainly is.

-

- While we might not lose sleep every night worrying about shipping lanes, it seems prudent to plan for the worst if the cost to diversifying shipping lanes is small.

Considering the latest National Security Strategy, the potential safety of shipping should be a consideration when building new facilities. That gives the nod to North, South, and Central America, especially if you are not already overly exposed to the region.

- What if the flow of processed or refined rare earths and critical minerals is cut off?

- Clearly this would be a risk if shipping with China is disrupted. But given what we’ve seen with the trade negotiations, it seems easy to play out scenarios where China decides to curtail shipments of their own volition.

These scenarios are by no means the base case, but do you really believe they have a zero probability of occurring? That there is no set of circumstances in the next few years under which China decides it is in their best interest to reduce shipments of these materials? Antimony is used in every munition and we remain highly dependent on China for this.

I am more focused on the refined and processed versions. China controls about 60% of the extraction/mining of what is broadly categorized as rare earths and critical minerals. They control about 90% of the processing and refining.

They can shut us off from the raw resources, but we could, in most cases, source them elsewhere. However, what good does it do if we have to ship them to China to be refined and processed?

I know I don’t always do a good job of highlighting the importance of these “things.” It is almost easy to dismiss some as they are “only a small part” of a bigger item. When we think “big picture,” it is easy to forget the importance that these little parts play in the grand scheme of things. Often, they are not just a little portion, but a large portion – when you are talking about batteries for instance.

With the help of OpenAI I have tried to bring the CEO of Whirlpool’s comments (made during COVID) to life.

This is maybe too “casual” or even too “obvious” as of course a washing machine needs a door, but that doesn’t make the point irrelevant (just my choice of graphics).

So much of our industrial production could grind to a halt, just because some small amount of processed/refined rare earths or critical minerals (that we depend on China for) doesn’t make it to our factories. It doesn’t only have to be to our “domestic” factories; this applies to factories anywhere around the globe, maybe even within China, if they decide to go down this path.

Again, it isn’t our base case, but becoming more RESILIENT, aka ProSec, goes a long way towards mitigating this risk.

While we don’t need to be completely “self-sufficient,” the more we can produce on our own, the more likely China won’t try to cut us off.

- Clearly this would be a risk if shipping with China is disrupted. But given what we’ve seen with the trade negotiations, it seems easy to play out scenarios where China decides to curtail shipments of their own volition.

-

Energy and electricity production.

We need to think about resiliency. We need realistic and cost effective contingency plans. The “irony” of this is the more independent one becomes, the less chance one becomes the target of an adversary or competitor. It is effectively Economic Deterrence.

Maslow’s Hierarchy of Economic Needs

Of all the things I learned in college, being able to open a bottle of beer with another beer and Maslow’s Hierarchy of Needs might be the two most useful things I learned (though to be honest, growing up in Canada, I think we learned the beer bottle thing in high school, but I digress).

I don’t know what “self-actualization” really is, but Universal Basic Income seems right up there. I previously thought we were in the “Esteem” stage. That let us think about things differently. The concern I have is that we were being overly “altruistic” in our vision because we thought we had the levels below us covered. The crumbling foundation is what has become apparent, first gradually, and then suddenly.

We have published on many of these themes going back to 2018. They aren’t completely new.

COVID did change a little of how we think and behave, especially towards China.

The Biden administration saw the need for the CHIPS ACT.

But all of these things seemed more like an attempt to patch a crack, rather than determining that the entire foundation might be crumbling and needs to be completely redone!

ProSec and ESG are Compatible

Despite how the previous section might come across, much of what “we” were trying to achieve with ESG will remain in place. But the lens through which we look at ESG will be changing with “true” Sustainability (Resiliency, Independence, Security, etc.) taking center stage.

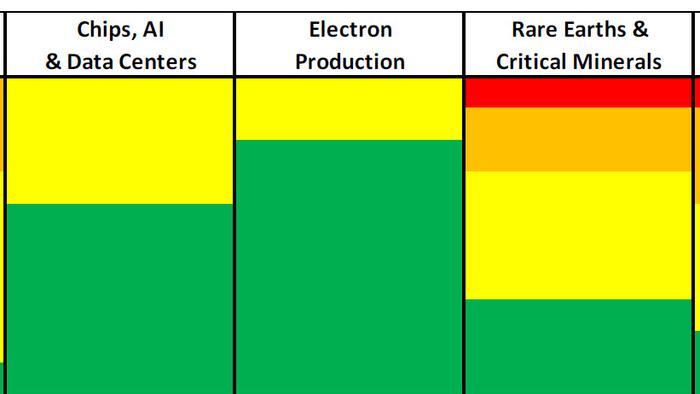

The ProSec Industries.

Let’s take a “quick” look at how we see the ProSec economy developing around specific industries.

This chart is intended to do a few things:

-

Make you wish that I’d figured out how to use AI to make this chart more professional.

-

Highlight the industries with some sense of relative importance (column width).

-

Highlight how much can be done easily (green), with some effort (yellow), facing some real hurdles (orange), and some that might not be achievable (red).

Biotech and Pharma.

-

As a “talking point,” reducing healthcare costs is easy. The complexity of the system makes it difficult. Same for “manufacturing at home.” On the surface it is “easy,” but there are a lot of difficulties. Hundreds, and even thousands of drugs are produced. We can kind of get away with saying “steel” and it covers the topic reasonably well (though purists would argue about the type of steel, etc.). But “drugs” is just too vague. There are the components, the base, and precursor drugs. There are the complex drugs we actually ingest or take. There are drugs with multiple delivery methods. The delivery methods themselves are sometimes separated from the drug itself. Patents. There is a focus here, but it is so complex that I think only slow progress will be made.

-

For the “green” section of this industry, look no further than the GLP-1 drugs. They have the benefit of being topical and potentially have incredibly widespread application. Certainly, interest in them is widespread. The combination of “big and public” makes them an ideal candidate for an administration to focus on. Lots of headlines and manageable. Away from that, it seems like it will be a slog to get a lot of manufacturing done here. It will happen over time (we had immense success getting the COVID vaccines produced here – regardless of your view on the vaccines themselves).

-

My best guess is that the admin will focus on the pharmacies next, rather than the manufacturers, as that industry is concentrated, and well known to the public, so easier to get a lot of “bang for the buck” on the political front. While I think this is an incredibly important ProSec industry, I think it will not be front and center in 2026 for opportunities.

Chips, Data Centers, and AI.

-

These industries are doing incredibly well in their own right. Demand is there. In terms of ProSec™ the goal of the administration will be to bring more and more production home. There are a lot of opportunities in this space. The industry leaders should continue to do well and get government support. That support might come in many forms. Some of it may be through increased government use of the services. The government (in all facets, including state, local, defense, and healthcare) will spend in this sector.

-

Regulatory help is another avenue the government will pursue. Whether paving the way for data centers, the power generation required, or even allowing products to be exported, to earn money, and to fund domestic growth, there will be support from the administration.

-

INTC continues to stand out in this sector. While I would like rules in place to regulate state investments, those are not really in place (and would likely be pushed to the limit by this admin, even if they were in place). I find it difficult to see a world where the government doesn’t try to support the taxpayers’ investment in this company. For full disclosure, INTC was my biggest single stock holding in 2025 and will be again in 2026. It was up 86% in 2025. Can it repeat that? Who knows, but while I think any stock in this space has potential, with those focused on manufacturing in the U.S. getting the most government support, the direct investment leads me to suspect that extra support will be given here.

-

Much of this chart is “green” and even “yellow” as a lot remains in our control. Look for a “shift” in the industry as it moves to where the energy (electricity) and fresh water are located. Tasks that require low latency will remain in locations that can offer that speed, but applications that allow for more latency will move to where the electricity is.

-

The administration is likely going to take a closer look at quantum computing. I briefly pulled up WQTM (a quantum ETF) and some of their holdings jumped out at me – QBTS, IONQ, RGTI, and ARQQ to name a few. I have not spent much time on this, but some of these stocks seem to fit the “lottery ticket” theme in ProSec™ (companies with a small enough market cap, that a direct investment by the U.S. taxpayers could help the stock “pop,” similar to the investment in MP – though that stock is well off of its highs).

Electron Production.

-

There will be a focus on not only producing the electricity needed for AI, Data Centers, EVs, and industry, but also getting it to where it needs to go (transmission).

-

All forms of electricity generation will be used. Okay, maybe all forms other than wind, which this administration seems to really dislike.

-

Fusion. This is more the “future” and I haven’t poked around for tickers, but makes sense.

-

Fission. This is an area we have focused on a lot. The government is clearly promoting the growth of the nuclear power business. From allowing nuclear to be built on Army bases, to chatter about using Navy reactors more broadly, the government is working hard to jumpstart the nuclear industry. It has the longest lead time to build. There remains a “fear” factor associated with nuclear (I wonder what the world would look like had the nuclear industry hired the Bitcoin marketing team ). Despite those risks (too long and too much negative public opinion) I think the opportunities remain very good in this space.

-

URA is an ETF that focuses on Uranium. One way to bet on the rise of nuclear, here and abroad (Canada for example is ramping up efforts in this area), is through Uranium. The commodity itself, the miners, and the refiners could all do well if the nuclear industry really takes off. Worth looking through the holding of ETFs like this to assess what stocks might make sense.

-

Personally, I’m fascinated with the Small Nuclear Reactor space. It has been a roller coaster ride, and we need to see projects completed, in scale, but this fits our theme extremely well.

-

-

Coal and Natural Gas. While nuclear might become the backbone years from now, we are going to need rapid expansion of coal and natural gas burning facilities. Maybe not as clean as “we would like” but it is necessary (ProSec™ is trumping ESG – pun intended). Companies like GEV will continue to do well as will other companies that can step in and produce turbines and other equipment that these facilities will need. That industry compressed, as it was out of favor with “traditional” ESG, but will do well again as we try to harness all sources of electricity production.

-

One of the issues with coal and nat gas is getting it to where the electricity generation is. It is often one of the more difficult logistical issues that companies face when developing new facilities (less so when increasing size of existing facilities). It is right up there with regulatory approval, which remains an issue. So, maybe we will build the facilities where the resources are? We mentioned this earlier and will mention it again. When generating power for a city, you cannot really move the city. When generating power for something like a data center, maybe building the data center close to the power source is best?

-

-

Solar. From all the discussions I’ve had, it seems difficult to see the admin suddenly agreeing that wind is necessary. On solar, there is that real possibility. It seems impossible to believe that the electricity production industry isn’t telling the President and his team that solar needs to be part of his overall plan. Elon Musk literally tweets about the need for solar almost every day. While the solar plays may not have the upside of say nuclear, they should have less downside. Since they are “under-owned” as the government cuts back on subsidies, they could actually surprise to the upside. I like some of the more solar-focused companies.

-

Transmission and the Grid. We will need to make improvements to our transmission lines and the grid. Not just in terms of capacity but also “hardening” it – better cyber- threat security and possibly even better physical-threat security. Companies involved in transmission and the grid should do well.

-

Batteries. The use of batteries is only going to increase (especially if the admin reverses course on solar, where battery power is more of a necessity, due to the potential timing mismatches of power production versus use).

-

Utilities. Unregulated utilities probably have the edge here as more “traditional” utility users (individuals like you and me) are becoming concerned, perturbed, or even angry about the use of electricity by the AI/Data Center business.

-

Much of this sector is green and yellow as so much is in our control. Regulations might be the biggest hurdle to achieve the power needs, but I expect that hurdle will be lowered in an effort to ensure that the U.S. wins the AI and Data Center race.

-

-

Rare Earths and Critical Minerals. I need to connect with Michael Rodriguez, Academy’s Head of Sustainable Finance (where he has always focused on resiliency), to do a more thorough dive into this sector – plus this report is already getting long for you to read, and my fingers are starting to hurt from typing so much. We are trying to analyze the importance of the material, alongside potential commercial application/profitability. Some are crucial to the U.S. but not viable domestically. The reason this sector has some orange and red coloring has less to do with the “willingness” and more to do with the “ability.”

-

Commodities. Similar to the above section, but with a lower priority. First, we need to “fix” our rare earths and critical minerals problem, then we can focus on commodities more generally. Some will get done, but that won’t be the highest priority. Again, focus on refining and processing over extraction. Commodities have less green and more yellow and orange than rare earths – precisely because the will and urgency aren’t there.

-

I like the “servicers” better than the producers. The producers should do well, but if ProSec works properly, other areas should too.

-

-

Heavy Industry. Steel. Aluminum. Chemicals. Nice to have, but gets complicated quickly. Also, project lead time is typically at the long-end of the spectrum. This seems more like a Phase 2 ProSec™ idea rather than something that will create immediate opportunities.

-

Defense. I will defer to our GIG members to opine on this more fully, but there will be a lot of opportunities with small/private companies developing “cutting edge” technology. There will remain a place for the “platforms” (aircraft carriers, state of the art fighter planes, etc.), but there are indications that drones, space, and anything autonomous are going to be the big beneficiaries of a Department of War that is to some extent repositioning itself (if not reinventing itself).

-

Ship Building. We need to make more ships. The U.S. Navy (as per my latest understanding) has plans to grow its fleet, albeit by small numbers. But despite that “plan,” the size of the Navy has been decreasing as ships are being retired faster than the replacements are being built. That is just the “traditional” Navy. Surface and underwater drones are going to play a major role going forward in shore defense (and attack). The Jones Act prevents non-U.S. built and flagged ships from shipping goods and commodities between two U.S. ports (one reason the Northeast imports a lot of gasoline while the South exports a lot of gasoline). I’ve been told the President doesn’t like the cruise ships in and around Florida (where he regularly sees them) flying foreign flags (on non U.S.-made ships). This industry is poised for government support.

-

Despite that rousing endorsement of this industry, very little is in green or even yellow. This will be a HEAVY LIFT. The skills, the materials, and the facilities are not readily available. This is more complex than ramping up electricity or getting a mine up and running. There are a lot of problems, not just hurdles, and shortages of skill and expertise will make this one more difficult to achieve. That could slow the admin down, as there isn’t quite the “easy” win we can see in some other areas. Yet it is critical and the “photo op” of breaking a bottle of champagne across the bow of the first ship built in a new yard would be impressive (though I suspect it will be the next President who would get to do that, given the time it is likely to take).

-

There are ways to invest in this sector, some of which would include defense stocks. I will also toss out BC (which I own) as a potential fit – especially if I’m correct on surface drones and other small watercraft being part of the defense plan going forward.

-

Maybe Ship Building should have just been a subset of Defense? Probably, but it probably deserves its own special section (and I don’t feel like re-organizing everything).

-

-

The Big Industrial, Transportation, and Infrastructure Companies. If we are even remotely correct on the importance of ProSec™ the build out will allow many companies to prosper.

-

While it might take time to get many projects on line, the build out will create jobs and wealth immediately. From railways, to massive vehicles, to pipelines, to equipment makers of all types, the opportunities will be there. The jobs and wealth will start with those building the facilities, as much as with the final projects. Accelerated Depreciation works great with this concept.

-

The X, Y, and Z of America First

I’m losing steam quickly (and I assume you the reader are too). So, we won’t belabor the point.

X is what can be done domestically and “reasonably” efficiently.

-

X will be a different percentage for each and every resource. Maybe in the U.S. potash can grow from the 10% range to the 25% range? But how much beyond this? There are limitations on how much can be produced domestically. While bananas are not part of ProSec™ we learned from tariff policy that it was kind of pointless tariffing them since we couldn’t supply significant quantities ourselves. While the goal might be 100% – that is highly unlikely. X also kind of represents the green and yellow in the charts above.

-

X will vary by country. Yes, today’s T-Report has been very focused on the U.S., but each country is headed in this direction and how much of a given thing you can produce yourself will vary greatly.

Y is what likely needs to be done in conjunction with partners.

-

Some things are just not available domestically.

-

Some things, while available, may be prohibitively expensive.

-

Economies of scale exist for a reason.

-

America First is NOT the same as Only America

-

Australia is striking deals with the U.S.

-

As USMCA negotiations begin, there are many clear and easy paths to see the U.S. working with Canada and Mexico (independently or collectively) to achieve ProSec™ related goals.

-

America First is the X. America not alone, is the Y.

-

Z is whatever is expedient.

-

Some things will be purchased as they fit the need. For some things, that may need to be very small. The size of Z will depend on the importance of the item and the relationship with the country producing the item.

-

It also allows me to revert from zee to zed depending on the audience.

There still will be plenty of global trade, but for ProSec related items, that trading relationship will be anything but transactional. It will be part of an overall plan to achieve true sustainability and resiliency.

Sovereign Wealth Fund

D.C. has gone quiet on the potential for a sovereign wealth fund. Can the idea of selling gold at spot prices to create “income” that can be invested in American companies get traction again? I certainly think so. I’d rather have that than a Bitcoin reserve.

Bottom Line

ProSec or Production for Security will:

The one “sad” truth is to some extent all we need to do is look at how China has shaped their economy, and we have a pretty decent roadmap for what we need to do. It will vary by country, by company, and asset manager, but ProSec™ will be a dominant factor in 2026.

The exciting part is that it incorporates AI and Data Centers (because you cannot ignore those industries) and it also sets us up for a pivot or rotation into new sectors and companies and should spur a wave of not just M&A activity, but also a lot of private equity activity as well!

Loading recommendations…

Read the full article here